Navigating the Rising Cost of Retirement in 2026

The transition from a steady paycheck to a fixed income is often met with the realization that inflation does not retire. For many seniors, the challenge lies in the fact that essential costs like healthcare and housing tend to rise faster than the standard cost-of-living adjustments provided by Social Security. This guide explores the modern landscape of retirement spending and provides a roadmap for maintaining financial dignity in an era of fluctuating economic pressures.

Essential Summary

Managing retirement today requires a shift from passive accumulation to active cash flow management. By prioritizing healthcare coverage, evaluating the equity held in personal property, and exploring secondary markets for underutilized assets, retirees can build a resilient safety net. Success depends on a combination of regular budget audits and the willingness to pivot when market conditions change.

The Impact of Modern Inflation on Seniors

Inflation acts as a silent tax on the retired population. While younger workers may see wage increases that offset rising prices, those on fixed incomes must find ways to stretch every dollar. Government data provides a clear picture of expenditures for people over sixty-five, which shows that essential costs represent a larger share of the budget than for younger cohorts. This reality makes it vital to understand specific strategies for managing spending to ensure that the longevity of your portfolio matches the longevity of your life.

Healthcare remains the most volatile variable in this equation. From supplemental insurance premiums to the out-of-pocket costs of long-term care, these expenses can derail even the most robust financial plans. Addressing these needs early through dedicated savings or specialized coverage can prevent a crisis later in life.

The Dynamic Withdrawal Architecture

To combat the erosion of purchasing power, many experts now recommend the Dynamic Withdrawal Architecture. This model moves away from the rigid four percent rule. Instead, it suggests adjusting your annual withdrawals based on the previous year’s market performance. When markets are down, you tighten the belt. When they are up, you can afford to cover those rising property taxes or home maintenance fees. This flexibility ensures that you do not deplete your principal during market downturns.

Rethinking Housing and Daily Costs

Housing is often the largest expense for retirees. Whether it is a remaining mortgage or the increasing costs of utilities and property upkeep, your home can become a financial burden. Some retirees choose to downsize to more efficient living spaces, while others utilize home equity to manage liquidity. It is helpful to review retirement security and income reports to see how different housing choices and debt levels impact long-term cash flow.

- Evaluate the necessity of high-maintenance properties.

- Consider the proximity to quality healthcare facilities.

- Analyze the tax implications of relocating to a different state.

- Investigate energy-efficient home upgrades to lower monthly utility bills.

Strategic Liquidity and Asset Optimization

Sometimes, traditional income sources like pensions and Social Security are not enough to cover a sudden spike in living costs. In these instances, exploring the secondary market for assets can provide a much-needed influx of capital. For example, some seniors find that a life insurance policy purchased decades ago is no longer necessary for their beneficiaries.

Exploring the option of selling a life insurance policy can generate immediate cash that helps cover rising healthcare, housing, or daily living expenses. It is important to weigh the loss of the policy’s death benefit and seek professional guidance before making a decision. You should consider working with a life settlement broker who represents policyowners as a fiduciary by managing the entire process. These professionals seek competitive offers from anyone who buys life insurance policies by engaging multiple buyers with no upfront fees. They typically only earn a commission upon closing, and you retain the right to cancel the transaction at any time.

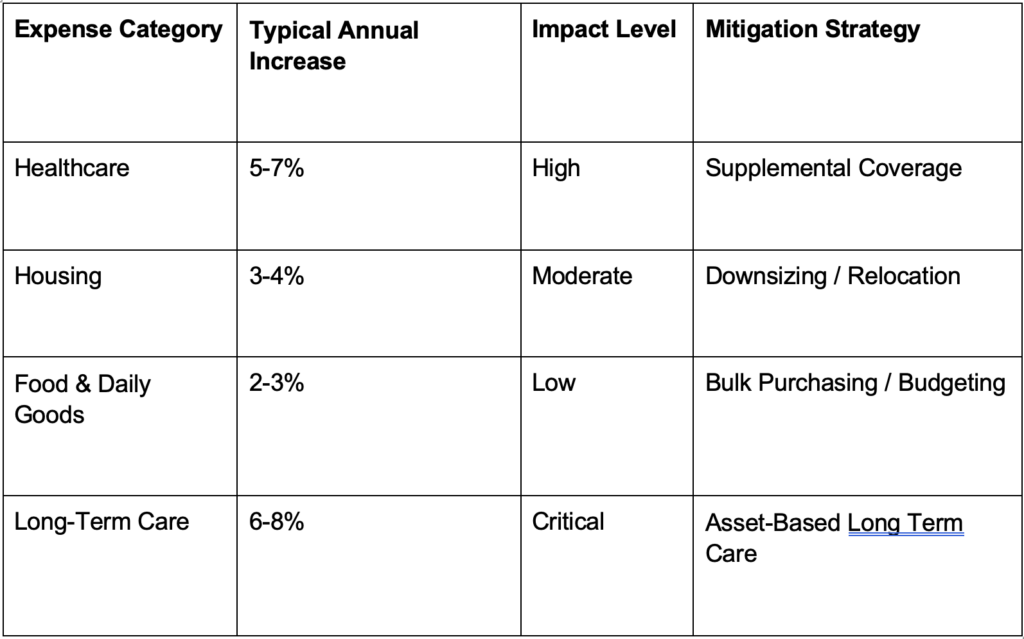

Comparing Retirement Cost Factors

Proactive Financial Review Checklist

To stay ahead of rising costs, a structured approach to your finances is necessary. This checklist provides a path toward sustained stability.

- Conduct a full audit of all subscription services and recurring monthly bills.

- Review your Medicare enrollment options annually to ensure you have the best coverage for your current health status.

- Consult with a tax professional to optimize the timing of your required minimum distributions.

- Examine research on retirement spending patterns to benchmark your own expenses against national averages.

- Rebalance your investment portfolio to ensure a proper mix of growth and income-generating assets.

Adapting to Economic Shifts

Economic conditions are never static. A strategy that worked five years ago may not be sufficient today. By staying informed on factors influencing retirement security as published by academic institutions, you can make adjustments before a small deficit becomes a larger problem. Flexibility is your greatest asset. Whether that means taking on a part-time consultancy role or finding new ways to utilize your existing assets, being proactive is the key to a stress-free retirement.

Monitoring your local economic environment also plays a role in your financial health. There is a strong correlation between geographic location and financial stability, as evidenced by senior economic security data that highlights the variations in poverty risks and utility costs across the country. Investing in knowledge today can save thousands in avoidable expenses tomorrow.

Frequently Asked Questions

How can I protect my retirement income from inflation?

Protecting your income involves diversifying into assets that traditionally perform well during inflationary periods, such as inflation-linked bonds or dividend growth stocks. Regular budget reviews and the use of the Dynamic Withdrawal Architecture also help in maintaining purchasing power over time.

What are the best ways to lower healthcare costs in retirement?

Lowering healthcare costs starts with selecting the right Medicare coverage during open enrollment. Additionally, maintaining a healthy lifestyle and utilizing preventative care can reduce the need for expensive emergency interventions or intensive long-term treatments that are often not fully covered.

When should I consider downsizing my home?

You should consider downsizing when the cost of maintenance, taxes, and insurance exceeds a comfortable percentage of your monthly income. Downsizing not only reduces expenses but can also unlock home equity that can be repurposed to cover other essential living costs.

Is it possible to change my withdrawal rate after I start?

Yes, you can and should change your withdrawal rate. Adapting your spending to reflect current market conditions is a hallmark of a successful financial plan. Seeking advice from a qualified fiduciary can help you determine a safe path for adjustment without risking the longevity of your funds.

What should I look for in a life settlement broker?

A reputable broker should act as a fiduciary, meaning they are legally obligated to act in your best interest. They should provide transparency throughout the process, secure bids from multiple reputable buyers, and operate on a commission-only basis with no upfront costs to the policyholder.

Conclusion

Securing your future requires a vigilant eye on the horizon and a willingness to adapt. By utilizing the tools and strategies outlined here, from the Dynamic Withdrawal Architecture to strategic asset optimization, you can navigate the rising costs of retirement with confidence. Forward planning and regular reviews will ensure that your golden years remain truly golden.

Article by Robert Schmitt